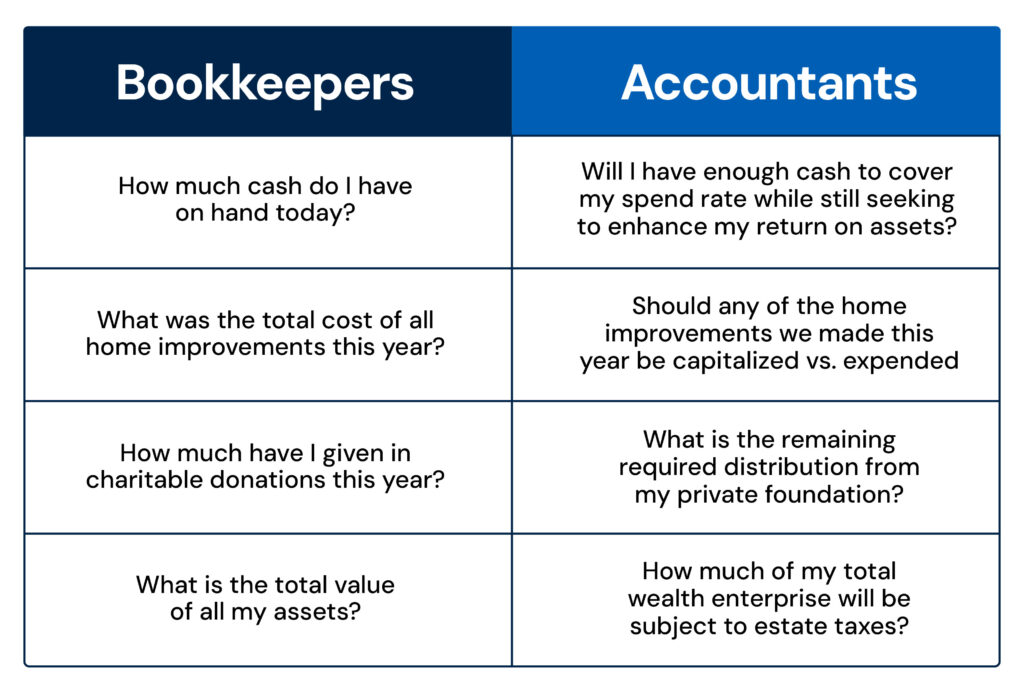

Many affluent families believe that their financial affairs are straightforward, leading to frustration over the lack of immediate access to comprehensive financial information for liquidity, budgeting, tax planning, and investment management purposes.

In reality, however, many wealthy individuals have more complex financial affairs than they realize, including multiple trusts, extensive private equity investments, private foundations, multiple residences, family limited partnerships, intrafamily loans, and much more. Given this complexity, one might question whether their financial affairs are truly as simple as they initially appear.

To keep track of it all, many wealthy individuals and families hire professionals to manage their finances. However, some families find that the inputs tracked through extensive bookkeeping are not the same as the insights provided through in-depth accounting and comprehensive financial reporting. This article will detail the tasks performed by each discipline and why both bookkeeping and accounting services are essential for providing structure and clarity to a family’s or an individual’s financial affairs.

Understanding the distinction between bookkeeping and accounting is crucial for holistic financial management. Bookkeeping involves the meticulous recording of financial transactions and documenting every financial move accurately. Accounting, on the other hand, encompasses a broader range of services, including the interpretation, analysis, and reporting of financial data to inform strategic decisions. Both functions are indispensable; bookkeeping provides the foundational data, while accounting transforms this data into actionable insights, enabling families to preserve and grow their wealth across generations.

Consider the example of a wealth holder with a diverse portfolio of personal property, marketable securities, and alternative assets. The bookkeeper enters all transactional data for a given month into a general ledger system and runs a few reports – perhaps total expenses, an income statement, and a balance sheet. But a monthly summary of debits, credits, liabilities, and assets doesn’t provide truly insightful information.

An accountant, however, will review the reports and:

As you can see, the bookkeeping data serves as the foundation for various analytical and strategic activities, but it requires a higher level of analysis to bring meaningful insights to the forefront.

For high-net-worth individuals with multiple family members, investment advisors, operating entities, residential properties, and staff it is often difficult to ensure that the appropriate tax deductions are being taken and reported correctly.

For example, many wealthy families have employees that support their personal needs from a lifestyle management perspective, but those same individuals may also provide support for the family’s business and investment-related activities. A bookkeeper might book a personal assistant’s payroll and benefits costs, for example, under a single entity in the general ledger. An accountant, on the other hand, might allocate a pro-rata share of those costs to the operating business or investment entities the assistant supports, thereby facilitating additional tax deductions for the family.

Additionally, while individuals may intend to keep all business-related expenses on one credit card and personal expenses on another, business and personal expenses are often intermingled. Most bookkeepers won’t know how to analyze the expenses and reclassify them as necessary to the tax-deductible business accounts, but a knowledgeable accountant will.

Ultra-high-net-worth individuals and their families face unique challenges in estate and wealth transfer planning. Accountants leverage financial records to develop comprehensive estate and wealth transfer plans that align with the wealth holder’s long-term goals. These plans might include charitable contributions, funding trusts, and direct gifting strategies. Bookkeepers record past actions, but accountants can help the wealth holder make more informed decisions about the future.

For example, while many bookkeepers will record an asset at cost upon its acquisition, they often won’t know the importance of tracking each asset under the appropriate entity’s general ledger account and continuing to record the fair market value of the asset on the balance sheet. As a result, the wealth owner may not be able to easily see where their personal net worth stands, especially regarding the value of assets still titled in their name. Without this information, it’s very difficult to answer questions such as “What is my estate tax liability if I were to pass away today, and what can I do to lower that in the future?”

Similarly, accountants will bring the wealth holder ideas that make current wealth transfer plans more efficient. For example, an accountant may know that an irrevocable grantor trust has a clause allowing for the exchange of an asset in the trust for an asset of equal value on the wealth holder’s personal financial statement. With such knowledge, they might recommend a swap for significantly appreciated marketable securities being held in trust with other non-appreciated assets of the same value. This way, beneficiaries get a step-up in basis upon the wealth holder’s death, which would not be the case if they were titled to a trust upon death. Learn more here.

Accountants can see trends in the financials and know that there are deeper questions to ask. For example, if the family owns a property that they usually rent out, but suddenly rental income stops coming in, the accountant is likely to raise questions to stay in compliance with tax regulations. Sometimes, a family member or friend is allowed to stay at the property for free, which the IRS classifies as a gift. If the rent isn’t reported on a gift tax return, then the statute of limitations doesn’t start running, and the IRS can go back and audit records indefinitely.

The same issue can apply to an intra-family loan. A bookkeeper may just book the payment as a distribution, but an accountant will know that additional documentation is required to ensure that the IRS doesn’t deem the loan a gift, potentially creating a 40% gift tax liability on the value of what was intended to be a loan.

Finally, an accountant will know to document not just the initial investment in a private placement investment, but the full amount of the uncommitted capital. Aggregating the uncommitted capital across the entire portfolio will enable better liquidity planning in the future as capital calls come in over time.

Questions about your wealth that bookkeepers and accountants can address:

Bookkeepers provide an essential service for affluent individuals and their advisors by maintaining accurate and detailed financial records. However, accountants take this data to the next level, transforming it into strategic financial planning, enhanced tax strategies, and a smoother generational wealth transfer. By leveraging the combined strengths of bookkeepers and accountants, affluent individuals and their advisors can enhance their financial management strategies and explore potential new opportunities for wealth growth and preservation.

Understanding the distinct roles and value of each professional is important for fully leveraging financial data. Whether focusing on accurate bookkeeping or benefiting from comprehensive accounting services, engaging the right professionals can provide the insights needed to grow and protect a family wealth enterprise for years to come.

Written by Nickie Dupuis. Copyright © 2025 BDO USA, P.C. All rights reserved. www.bdo.com

“SSC CPAs + Advisors” and “SSC” are the brand names under which SSC Advisors, Inc. and SSC CPAs, PA provide professional services. SSC Advisors, Inc. and SSC CPAs, PA practice as an alternative practice structure in accordance with the AICPA Code of Professional Conduct and applicable law, regulations, and professional standards. SSC CPAs, PA is a licensed independent CPA firm that provides attest services to its clients, and SSC Advisors, Inc. entities provide tax, advisory, and business consulting services to their clients. SSC Advisors, Inc. is not a licensed CPA firm. Our use of the terms “our firm” and “we” and “us” and terms of similar import, denote the alternative practice structure conducted by SSC Advisors, Inc. and SSC CPAs, PA. Advisory services provided through Merit Financial Group, LLC. Merit Financial Group, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission.